Carro: Solving the Lemon Problem

Driving forward with data and machine learning.

In 1970, George Akerloff wrote a paper called The Market for Lemons.

Using the market for used cars as an example, he observed that markets with asymmetric information would degrade and eventually collapse.

Because buyers couldn’t differentiate between quality products and defective products (“lemons”), they would have to price in the chance that they would receive the latter to ensure that they were properly protected. As a result, honest sellers were less likely to sell their goods in the market since they would always be getting a worse price than they would elsewhere. Buyers would then have to price in the higher probability that they would receive a lemon, therefore starting a new feedback loop with more sellers in the market. This continues until the market is left only with lemons and eventually collapses.

Akerloff would later be awarded the Nobel Prize in Economic Sciences for his work on asymmetric information (that one paper alone earned him 41,500 citations). More importantly, governments around the world started passing consumer protection laws in all sorts of industries, requiring companies to provide warranties on certain consumer products. That allayed some of the problems caused by asymmetric information.

But the used automotive market - Akerloff’s example - remains unchanged. Consumer protection laws don’t address transactions where a consumer sells to another consumer, and in less developed countries, you have even fewer protections since it becomes too costly to enforce such regulations. It’s a huge problem, especially since cars are big ticket purchases.

That’s where Carro comes in.

Founded in 2015 by Aaron Tan, Aditya Lesmana, and Kelvin Chng, the end-to-end used car marketplace aims to make buying and selling a second hand car seamless and convenient. Using AI, Carro is able to do a 160-point inspection of a car in a fraction of the time it takes humans to do so. It then arrives at an optimal price based on identified defects and wear-and-tear as well as current demand for that model. And if someone is interested in making a purchase, Carro can provide financing as well.

The potential is huge, and investors have taken note. In June 2021, Carro became a unicorn after raising a US$360 million Series C led by Softbank. They followed that up with a US$100 million Series D led by Temasek later in December. That takes its total funding to over US$520 million from regional name investors such as Singapore’s EDBI, B Capital, Insignia Ventures, Golden Gate Ventures, and Alpha JWC.

All this is a lot of money, but as we’ll see, not excessive for an industry with such a massive TAM. In this piece, we’ll cover:

Origins: TAM was top of mind when Aaron Tan founded Carro. This has paid off as the company has avoided the slowing growth that plagues so many start-ups in SEA.

Product: Unlike some of its competitors, Carro has built out enough products to serve consumers in the entire purchasing cycle. This puts it in a great position to scale in the region and grab market share with its end-to-end solutions.

Business Model: Carro started off as a marketplace, but has evolved into a retailer. This has allowed it to infuse data into all of its operations, although it also creates new risks for the business.

Future: Unlike other car marketplaces which are doing terribly in this business environment, Carro has been profitable for a few years. This puts it in a great position to seize future growth opportunities as interest rates stabilise.

Let’s jump in.

Starting in Overdrive

Before Carro, Aaron had already built two businesses. None of them were at the same scale but it’s hard to blame him for that: Aaron was just a teenager.

At 13 years old, he started a network hosting company as the Internet was taking off. And at 16, he built a small search engine that made advertising dollars on a pay-per-click model. That was a time long before Google - Yahoo was just a direct feedback platform then, and there were other search engines such as Lycos, Excite and AltaVista.

Business was good but Aaron eventually sold his companies so he could focus on his studies. This would be an incredible experience in itself. Like Justin Kan and his co-founders, Aaron sold his first start-up on eBay. Unlike the eventual co-founder of Twitch, however, Aaron faced an additional legal problem:

“When I sold my first company, the buyer actually flew into Singapore and basically told the lawyers, ‘this guy is underage’ and that whatever had been signed would not be legally binding, which almost collapsed the deal, but it worked out in the end.”

Aaron went on to study computer science at the Singapore Management University and followed that with a Master’s at Carnegie Mellon under a government scholarship. After finishing his studies in 2010, he returned to serve his five-year bond with Singtel Innov8, the corporate VC arm of state-owned Singapore Telecommunications. But because there were so little investable deals in Southeast Asia, Aaron would spend most of his time in the US. The only time he spent back home was working on an initiative called Block 71 to build centralised office spaces for startups - an initiative that has since helped companies such as Shopback, Carousell, and Glints.

VC might be a dream job for many, but it wasn’t enough for Aaron. He didn’t want to just support entrepreneurs; he wanted to be in the driver’s seat. Nothing thrilled him as much as owning and running his own business and he wanted to recapture that feeling from his teenage years.

With technical skills and VC experience, the possibilities were endless. But Aaron knew right from the start that there were only two verticals that he would ever consider: property and cars. Both were huge markets and Aaron knew from his experience as a VC that a large TAM was crucial for building a large company. And then there was his Singaporean upbringing as well - property and cars were top of mind for anyone who lived in the island nation.

The tiebreaker came down to market momentum and competition. Grab was just taking off in 2016 and used car marketplaces were doing well in the US and China. Property on the other hand moved at a slower place. Beyond Airbnb, it didn’t seem like there was any innovation in the space. Portals such as PropertyGuru also existed and it was clear that any new entrant would be late to the game. It made more sense for Aaron to work on something that facilitated automotive transactions - it was an age-old problem and the timing was perfect.

Aaron called up two of his schoolmates and sold them on his idea. Both of them had spent time with Aaron at SMU and Carnegie Mellon, and they signed on. There was also something serendipitous about this team: Aditya Presmana had ties to Indonesia while Kelvin Chng had ties to Thailand - and between the three of them, they could cover the largest automotive markets in Southeast Asia. It was go-time.

The Road Taken

Carro initially launched as a consumer marketplace for cars.

Positioning themselves as an online marketplace that would disrupt how transactions were done, an explicit goal was to cut out the middleman and have consumers transact directly. Instead of selling your car directly to a dealership, Carro would send someone to inspect your car and provide a pricing estimate immediately before marketing your car through various channels. And if no one bought your car within 30 days, Carro would take it off your hands at the price they provided.

This worked, and Carro had over 100 transactions on their platform within four months of launching. It was an innovation on the business model, with lower costs across the board, including in storefront overheads and operational costs. Machine learning was also introduced, with algorithms trained on photos of cars that the company had serviced, with the goal of reducing the amount of time it took to carry out inspections. Off the back of such traction, they raised a US$712K seed round from a number of angel investors.

Growth continued to be impressive. At 30% month-on-month, they raised a US$5.3 million Series A round led by Venturra Capital, with participation from other investors such as Aaron’s alma mater Singtel Innov8, Golden Gate Ventures, and Alpha JWC. Singapore had been a great market with car values in the six figures due to Certificate of Entitlement (COE) prices, but they needed to expand regionally to continue growing.

But they soon encountered a problem: car dealerships were turning hostile towards them. In an industry which was opaque and where relationships mattered, the backlash started to obstruct growth. “Looking back, positioning ourselves as an anti-dealer brand to start was a bad idea”, Aaron admitted.

So they pivoted. Instead of cutting out car dealerships entirely, Carro would now buy used cars from consumers and then sell them to dealers through an action. This was a win-win. Dealers would get a new pipeline of inventory that they could flip without the hassle of having to conduct their own inspections. And on Carro’s end, it allowed them to buy vehicles directly from consumers and reduce the time it took for transactions to close since there was greater assurance that they could offload the cars that they had bought, even if other consumers didn’t purchase it on their platform.

Although it was meant to be an additional service called Carro Express, this new model was so successful that it would replace the C2C marketplace that Carro had been using. The team had initially been hesitant to make this switch and for a good reason: doing so would significantly increase capital and operating expenditure and create new risks for the business. But Carro’s (improving) AI-powered inspection capability meant that it was able to better price cars, which potentially translated to better margins on each car that they bought and sold. Managed well, the move would improve the economics of the business.

But that wasn't all. Aaron and his team also realised that it was difficult for some of their customers to get loans in a quick manner, and without the financing, it was impossible for most consumers to purchase their cars. So they did something that any good entrepreneur would do - turn that problem into an opportunity by launching their own financial services arm.

With the data gathered by Carro, they were able to more accurately price cars and loans, factoring in information that banks couldn't, such as the trade-in value of cars. “We built our own credit engine that allows us to underwrite loans in a different way than banks”, says Aaron. To fund the development of their credit operations, they raised US$12 million from existing and new investors.

The switch in business model, coupled with the launch of a financial services arm, would let the company cruise through the next couple of years. Growth never stopped, in terms of market expansion and product development:

Lending had become profitable with over US$100 million in loans processed

Partnerships with insurance underwriters meant that Carro could now directly offer car insurance to consumers

After-sale care, including roadside assistance, maintenance and purchase of gadgets, was now readily available through Carro branded workshops

They launched in Indonesia and Thailand, the two countries Aaron had initially identified as key markets they had to conquer

Investors took note, and in 2018, Carro raised US$60 million in a Series B round co-led by B Capital, Softbank Ventures Korea, and Insignia Ventures. Carro started experimenting with leases and a subscription product, which allowed users to swap out vehicles within a certain price tier, but phased it out after some time. They did however arrive at a new usage-based pricing offering, which adjusted the monthly payable on a car. More mileage on a car meant more wear-and-tear as well as a greater chance of accidents (and insurance payouts), and Carro’s analytics had become advanced enough that they could price these in as well. Product innovation never stopped.

Then Covid hit. People stayed indoors because of the pandemic, and no one was buying any new cars. And since no one was trading-in their cars, Carro’s wholesale business nosedived, and revenues from that segment dried up.

But Carro Leap, the company’s short term flexi-lease product, unexpectedly showed up as the bright spot. As the pandemic wore on and lockdowns became gradually lifted, more and more consumers wanted their own form of private transport and were willing to fork out the money for car leases. The demand was so strong that the company didn’t have enough inventory to fulfil demand and had to reach out to car dealerships for inventory to list on their platform. In the end, the additional revenue from Leap was large enough to negate the drop-off in its wholesale business during this period.

As markets recovered in 2021, Carro finally reached unicorn status with its US$360 million Series C round led by Softbank Vision Fund 2. In a sign of its future ambitions, it then took in another US$100 million later that year from a variety of large corporates and state-linked funds, including Singapore-based Temasek Holdings, Malaysian state-backed manager PNB, Japan-based Shinhan Financial Group, and Indonesia-based Emtek Group.

Big money, from established institutional investors. The kind of money that says something is legit. And it’s not hard to see why.

First, Carro’s revenue growth was strong, with earnings of US$225 million in 2021 and double that in 2022 at US$460 million. Second, in a time when startups were burning cash in the name of growth, Carro was profitable, proving that the unit economics worked. Lastly - and perhaps most importantly - the opportunity was still huge with tailwinds behind it.

All of this - along with the then-cheap capital - justified the valuation. But as we’ll see, there is a strong proven business model here as well which justifies the premium paid at this stage.

Carro’s Business Model

Carro’s business is split into three main verticals: retail, wholesale, and financing.

At the core, however, Carro’s revenue comes from the spread between the purchase price and sale price. This is then augmented by the various warranties that Carro provides based on the defects that it has identified and rectified, and through refurbishment of the vehicle. Finally, it then layers on various financial products such as car loans and auto insurance.

What makes all of this possible is Carro’s computer-vision inspection capability, which has been expanding since day one. Carro doesn’t make any money off this, although it does provide some operational cost savings. Its main utility, instead, is to provide a reason for consumers to pick Carro over other methods of buying or selling a car. By ensuring that no defect goes unnoticed, and then convincing everyone that this is the case, consumers and dealers alike come to Carro because they know they’re dealing with an honest broker. Put another way, solving the lemon problem is what allowed Carro to wedge into the larger automotive market.

But for the wedge to be effective, you need more than tech. Carro knows this as well, and is not just enhancing its AI/ML capabilities, but also communicating this. They launched Carro Certified in 2022, which is basically a report with Carro’s stamp of assurance on it. I don’t know how many of the 160 points that they look out for are vital, but as a consumer, I know that I’m being taken care of and nothing is missed. Others know that as well. This, uncoincidentally, is also what prevents a lemon market from being produced.

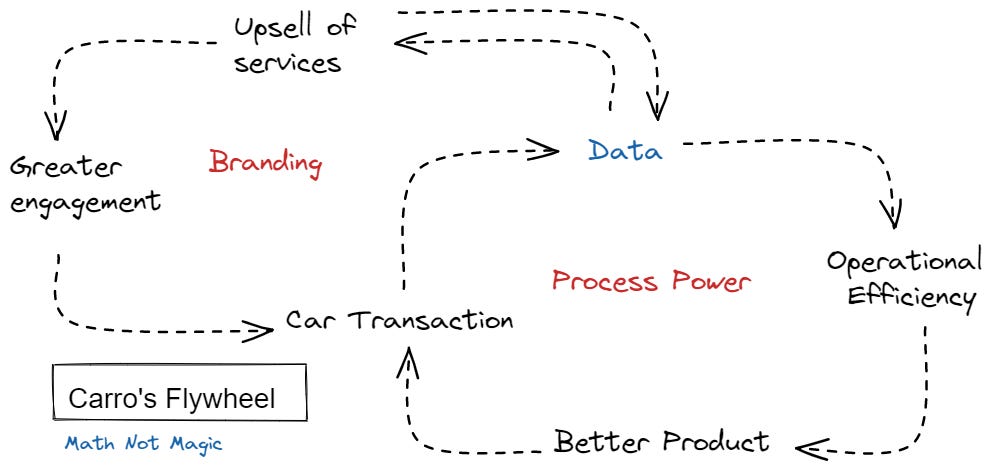

Beyond AI/ML, data analytics comes into play as well. Each time a buyer or seller transacts on the platform, Carro learns a little more about that individual and their transactional behaviour. This is the other piece of the puzzle that makes the Carro machine turn.

On one hand, Carro is able to identify what an individual might need based on the type of service they purchase. Financial products such as loans and insurance are obvious opportunities to increase customer LTV and capture more information, but things like frequency of car repairs and the mileage on a vehicle also help to paint a clearer picture of what kind of driver someone is.

On the other hand, all this information provided allows Carro to improve its operational efficiency. How should they price their warranty? Can they still sell a car at the same price with dampening consumer demand? What happens if an entire quarter’s worth of cars is stuck in the Suez Canal? Answering these questions improves the product that Carro puts in front of consumers and dealerships, which leads to more transactions and data. I’m probably missing a few things here, but the result is a flywheel that looks something like this:

Of course, this hasn’t come without a cost. Purchasing cars directly from consumers and then selling them, whether wholesale or back to consumers on its platform, means that Carro has significantly greater capital expenditure than if they were to allow buyer and seller to transact directly. Plus, there is also the risk that Carro isn’t able to unload their inventory profitably if demand weakens - it’s one of the reasons Carvana has seen its market cap fall by over 90% since its peak in 2021.

So far, Carro has done well to manage these challenges - cars typically stay in its inventory for less than 60 days. Its unit economics, however, reflects the reality of such capital expenditure. Gross margins on the retail side hover around 15%, although that might dip closer to the 10% mark after factoring in its wholesale business. While this is higher than competitors such as Carsome (5.6%), it's nowhere close to the software margins that VCs have come to love and expect.

Still, a vertical play appears to be the right move. Pure listing platforms don’t do a good enough job of attracting users, and horizontal marketplaces are untenable given the trend of unbundling such platforms. In contrast, margins will likely continue to improve as Carro’s flywheel takes off and it finds a way to expand into adjacent services.

Future

As with all startups, Carro’s plan is to continue expanding.

This makes sense: the used car market is large, fragmented, and generally a terrible experience for most users. There’s no reason to believe that such features are unique to any one country; after all, the lemon problem is not constrained by geography or culture.

Carro has acted accordingly. Acquisitions become more common as a company matures, but perhaps the most noteworthy so far has been Carro’s acquisition of Jualo in 2019, an Indonesian listing platform which derives 40% of its traffic from motorcycle searches. This reveals a deeper ambition: Carro not only plans to expand into more countries but also into new verticals as well.

The possibilities are endless. Motorcycles make sense because they are the most common form of transport in countries like Vietnam and Indonesia, which means that speedboats are likely on the horizon as well since Indonesia and the Philippines are archipelagos which comprise thousands of islands. But if we go back to the core problem that Carro solves (and use a great deal of imagination), it’s possible that Carro will facilitate any vehicle-based transaction that has an opaque market. Trucks, lorries, yachts, bicycles, e-scooters - these are all fair game.

Of course, not all of these will materialise, and those which do will have to operate on a tweaked business model. But if this is any sign of Carro’s ultimate potential, we’re in for a ride.

Thanks to Trevor for reading drafts of this.

Liked This Post?

Thanks for reading! If you liked this, drop your email below and get posts sent directly to your inbox when they are published.

And if you really love it, share this with someone else. It’ll make my day.